The critical test that any supporting business process must pass is ‘does this help the business become more efficient and effective?’

Administering a budgeting system is very costly and so can become part of the problem we are trying to solve. But even worse, budgeting – which has the aim of constraining costs – can promote behaviour that has the opposite effect.

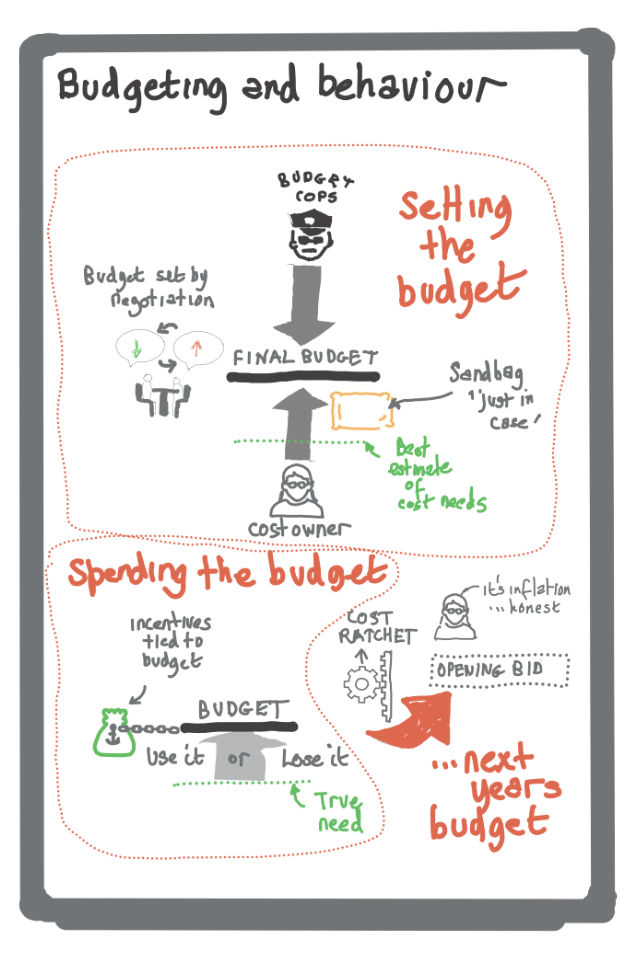

Here's why.

Cops and Robbers

Cost and profit centre managers are judged by their ability to eliminate or minimise variances. There are two ways to do this: reduce the amount spent, or negotiate higher cost budgets...and the latter is much the easiest route.

So, a key player in the system (the cost ‘owner’) is given an incentive to behave in a way that will actually increase costs, particularly if their incentives are tied to the budget number.

As a result, the already inherently complex budgeting process becomes even more bureaucratic. Cost centre managers are incentivised to submit bids for resources, not ‘honest’ estimates, (a process called ‘sandbagging’) and those administering the process are forced into the role of policemen, trying to spot and root out ‘bad’ behaviour.

Use it or lose it

Because no other company will have the same responsibility structure as your own, there is usually no objective external cost benchmark that can be used to guide the process.

This means that budgets are often set with reference to what has been incurred in the past.

As a result, there is an incentive for cost centre mangers to spend all their budget, whether they need to or not – to ‘use it or lose it’ in the jargon.

In these circumstances, budgets become to be seen as an entitlement – something that is owned by the budget holder that they can spend in any way they want. This has the effect of ratcheting costs up over time.

ZBB

To counter this, a variant of the traditional budgeting process called Zero Based Budgeting (ZBB) has recently come back into fashion.

Zero Based Budgeting was first developed in the late 1970’s and requires every single item of expenditure to be justified from first principles.

Even if you had the knowledge to do this properly, which is unlikely, since the process is often performed over a year in advance, it isn’t difficult to see why this is immensely more costly to administer and why it can supercharge the negotiating culture.

The result? The budgeting process often ends up incentivising behaviour that has the effect of increasing costs over time.

Extracted from "Cost Matters: How to manage without budgets and help lean and agile to fly" by Dr Steve Morlidge.

To learn more about how Beyond Budgeting fits together with other recent innovations such as Lean and Agile to create a coherent model for the organisation and regulation of work, buy your copy here.